marginal cost

!!!

In economics, when the quantity produced is incremented by one unit then marginal cost arises as it the change in the opportunity cost. We can also define Marginal cost as the cost of producing one more unit of a good.

It includes the cost of any additional inputs required to produce the next unit at each level of production.

other costs that do not vary with production are considered fixed whereas marginal costs include all costs that vary with the level of production.

Definition: Marginal cost is the additional cost occurred for the production of an additional unit of output. The formula is calculated by dividing the change in the total cost by the change in the product output which is depicted by formula as-

MC= TCn-TCn-1

Features of Marginal Cost:

1. It helps in taking managerial decision by the technique of analysis and managerial decision.

2. All the elements in marginal cost like Cost of production, administration and selling and distribution are classified into variable and fixed components.

3. The variable cost or we can say Marginal cost are regarded as the cost of the products.

4. Stocks like finished and work in progress are valued at Marginal cost only.

5. Fixed cost are treated as cost of period and when they occur they charge to profit and loss account.

MC is mostly useful in the business decision-making process. Where to best allocate resources in the production process so Management has to make decisions.

Let’s look at an example.

X is a Manufacturing company and manufactures electrical appliances. The factor’s old and obsolete technique of production does not meet the firm’s manufacturing needs and can’t keep up with the production schedule. The firm has to buy rent additional equipment to maintain its production at the same levels.

Thus, the management needs to calculate the marginal cost of the electronic appliances that will be produced by the new equipment, including the cost of their acquisition.

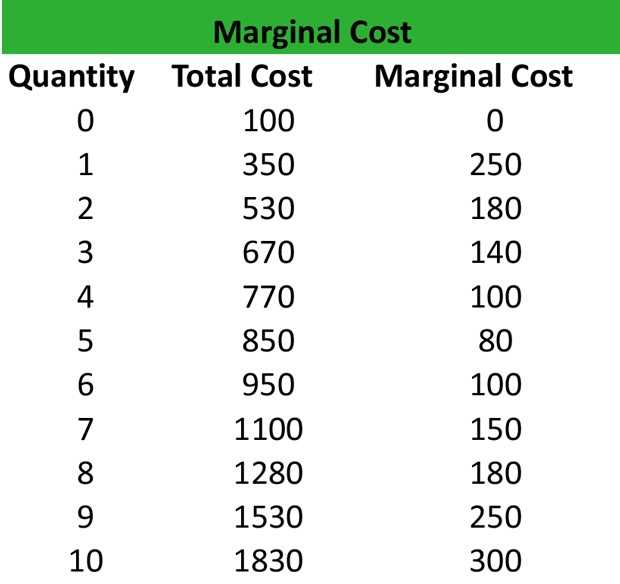

Observations

1. The total cost increases as the larger quantities of production factors are required then the quantity of the product increases

2. The MC is reduced up to a certain level of production ie., Q=5, and then, it keeps on increasing along with production.

3. The MC of producing an additional unit of electrical appliances at each level of production has to take into account a sudden rise in the raw materials.

The MC may increase due to longer distances and higher prices of raw materials, if the firm has to change its suppliers.

hope you understood the main idea!!!